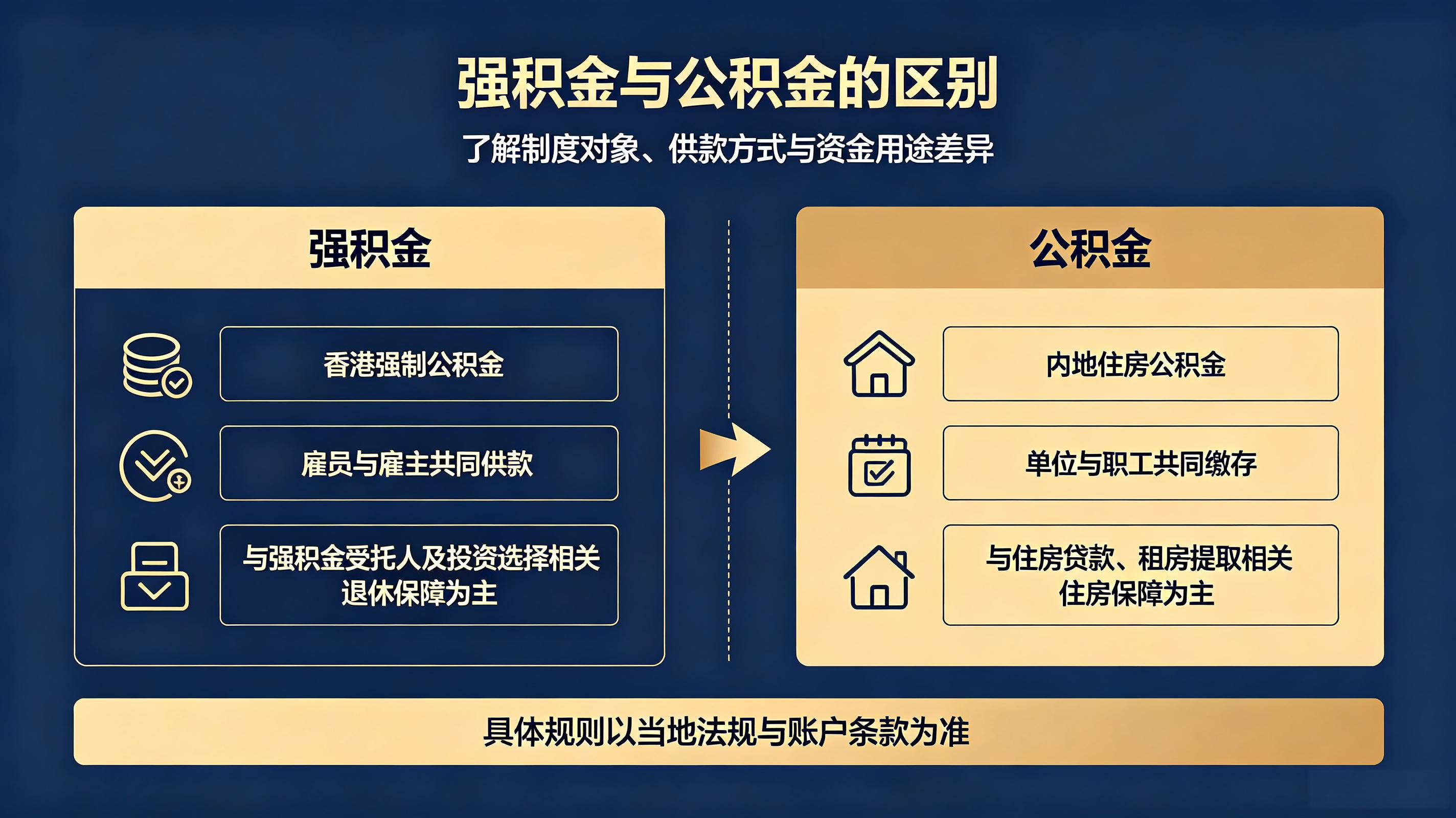

MPF vs Provident Fund: A World of Difference in Just One Word! An Article Explains It All

2026.07.30

On March 27, 2026, the Hong Kong government published the "Inland Revenue (Amendment) (Automatic Exchange of Financial Account Information) Bill 2026" in the Gazette, marking the official launch of the Hong Kong CRS 2.0 legislation. On April 1, the bill was submitted to the Legislative Council for first and second readings, and is expected to take effect from January 1, 2027. This marks a crucial milestone in global cross-border tax transparency.

01. What is Hong Kong CRS 2.0?

CRS, fully known as the "Common Reporting Standard," is a global standard for the automatic exchange of financial account information established by the Organization for Economic Cooperation and Development (OECD). Simply put, it involves the automatic exchange of financial account information of residents between tax authorities of various countries (regions) to prevent tax evasion through the use of cross-border financial assets.

The Hong Kong CRS 1.0 has been implemented since 2017, requiring financial institutions such as banks, securities firms, and insurance companies to collect account information of non-Hong Kong residents and submit it to the tax authorities of their tax residences.

Hong Kong CRS 2.0 is a fully upgraded version, featuring three major breakthroughs:

In a nutshell: CRS 2.0 leaves no room for cross-border assets, crypto assets, and multiple identity arrangements to hide.

02. In-depth interpretation of three core changes

Change 1: Cryptocurrencies are fully brought under supervision, marking the end of the "era of invisibility" for digital finance

This marks the greatest breakthrough in this legislation. Hong Kong has simultaneously implemented the OECD's "Crypto-Asset Reporting Framework" (CARF), explicitly incorporating the following assets into the definition of financial assets:

The scope of reporting entities has also been significantly expanded: crypto asset exchanges, payment institutions, custodian wallet service providers, etc. operating in Hong Kong must fulfill KYC (Know Your Customer) and information reporting obligations like traditional banks.

Special reminder: Even if you use a decentralized exchange (DEX), as long as you conduct transactions through a centralized entry point (such as a fiat currency deposit channel or a cross-chain bridge), relevant information may still be included in the declaration scope. Self-custody wallets themselves do not submit directly, but once an exchange occurs with the exchange, the records are collected.

Timeline:

From 2027 onwards, crypto asset service providers began to collect customer information;

From 2028 onwards, automatic exchange of information on crypto-assets will be implemented with eligible tax jurisdictions worldwide.

Change 2: Dual tax residents are prohibited from choosing between two options, and the benefits of cross-border identity have completely disappeared

Loopholes in the old regulations: For individuals who are tax residents of both the mainland and Hong Kong, they can choose to file tax returns in only one place based on the "look-through rule" of tax treaties, and financial institutions will only submit information to that place.

New and stringent regulation: Account holders must truthfully declare all their tax residency statuses, and financial institutions are required to synchronously submit the information to all relevant jurisdictions. For instance, if an individual is a tax resident of both the mainland and Hong Kong, their Hong Kong account information will be exchanged simultaneously to both the State Taxation Administration of the People's Republic of China and the Inland Revenue Department of Hong Kong.

Influential group:

Cross-border high-net-worth individuals

Investors in Hong Kong and US stocks

Cross-border e-commerce seller

Individuals who possess multiple passports or frequently reside in two different places

Cross-matching of information between tax authorities in two regions will become the norm.

Change 3: Penetration supervision is upgraded, and penalties are significantly increased

Penetrative information reporting: Financial institutions must submit:

Actual controller of the account (Ultimate Beneficial Owner, UBO)

Account status (newly opened/existing)

Specific roles within the investment entity

Mandatory registration system: All financial institutions and cryptocurrency service providers, regardless of whether they have declared accounts, must register with the Hong Kong Inland Revenue Department. Existing institutions must complete the registration before March 31, 2027.

Penalty escalation:

Minor underreporting: Penalty based on account;

Serious fraud and concealment: maximum fine of HK$500,000;

In severe cases: facing criminal charges + late payment fees of up to 18% per annum.

03. Which entities will be directly affected?

According to the latest legislative developments, the following five categories of entities will be directly affected by CRS 2.0:

Individuals and entities holding bank, securities, fund, and insurance accounts in Hong Kong and abroad

The actual controller who holds financial assets through offshore companies (BVI, Cayman, etc.)

The entity holding crypto assets (stable coins, NFTs, derivatives)

Individuals with dual or multiple tax residency statuses

Residence planners who need to determine their tax resident status in Hong Kong

The essence of CRS 2.0 is not to create panic, but to promote the evolution of cross-border taxation towards a more standardized and transparent system. For individuals holding cross-border assets, actively complying with regulations and improving the reporting process are the fundamental ways to safeguard their wealth.

*The content of this article is based on the public information from the Hong Kong Inland Revenue (Amendment) (Automatic Exchange of Information) Bill 2026 and the OECD CRS 2.0/CARF framework. Policies and regulations are subject to official announcements, and for specific implementation details, please refer to subsequent announcements from the Hong Kong Inland Revenue Department. *

The CRS 2.0 era has arrived in Hong Kong. Will your money be "taxed on both sides"? Cryptocurrencies, dual identities, offshore structures... All the issues you care about are here.

Next article News | 2026.07.30MPF vs Provident Fund: A World of Difference in Just One Word! An Article Explains It All

Please be sure to provide truthful personal information so that we can contact you more quickly