The CRS 2.0 era has arrived in Hong Kong. Will your money be "taxed on both sides"? Cryptocurrencies, dual identities, offshore structures... All the issues you care about are here.

Recently, the news that the Hong Kong CRS 2.0 legislation has been launched has spread like wildfire in the cross-border community. Cryptocurrencies will be included in the declaration process, and dual tax residents will no longer have the option of choosing between the two... Many people's first reaction was: What does this have to do with me? Will I end up paying more taxes? Don't worry. Today, let's clarify this matter with an article: Exactly what has been changed in Hong Kong's CRS 2.0? Has the Gabe rule really died? Do you really need to "pay taxes on both sides"? And what is the most important thing you should do now?

Let's start by answering the three questions you are most concerned about

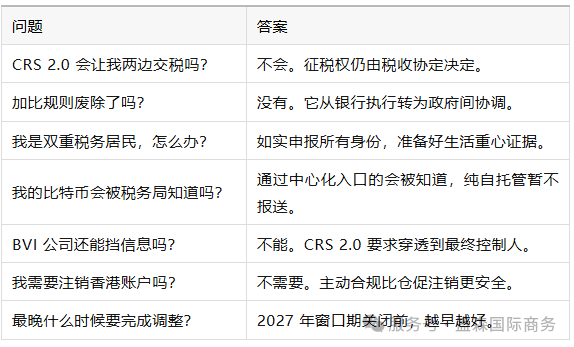

1. Will CRS 2.0 make me pay taxes on both sides? No. The essence of CRS is "information exchange", not "change of taxing rights". Your account information may be simultaneously reported to both the mainland and Hong Kong tax authorities, but ultimately who will be responsible for the taxation and how much will be taxed is still determined according to the "Arrangement for Avoiding Double Taxation" between the two regions. This set of rules has clear "rules for who should give way to whom" (the Gabi rules), and there will be no situation where both sides make concessions at the same time.

2. Is being a "tax resident" very risky? No, it's not risky. It just requires regulation. CRS 2.0 addresses the loophole of "binary choice" reporting. If you truthfully reported all your identities in the past, the impact would be minimal; if you only reported one side or didn't report at all in the past, you need to actively correct it now. The real risk is not double taxation, but the investigations and fines that come from concealing and failing to report.

3. Will the encrypted assets be known by the tax authority? It depends. Only in the self-hosted wallet and never interacted with the exchange: currently will not be reported. Transactions have been conducted on the Hong Kong Compliance Exchange since 2028: Information will be exchanged from then on. Through overseas exchanges but the deposit channel involves Hong Kong: The situation is complex. Professional consultation is recommended. The encrypted assets through centralized entry are losing their "cloak of anonymity".

I. What exactly is CRS 2.0?

1. The basic principle of CRS CRS (Common Reporting Standard) is a global standard for automatic exchange of financial account information. For example: You have rented a room at a hotel (Hong Kong Bank). The hotel will inform the local police station of your residence (the tax authority of your country of citizenship) of your stay. CRS 1.0 only records the room number and the name. CRS 2.0 will also ask you about the luggage you are carrying (encrypted assets), the number of your identification cards (multiple identities), and whether the person who helped you book the room is your friend (offshore structure).

2. What does CRS 1.0 cover? Since 2017, Hong Kong has implemented CRS 1.0, and the main exchanges include: Bank deposit account Securities account (stocks, funds, bonds) Insurance policies with cash value.

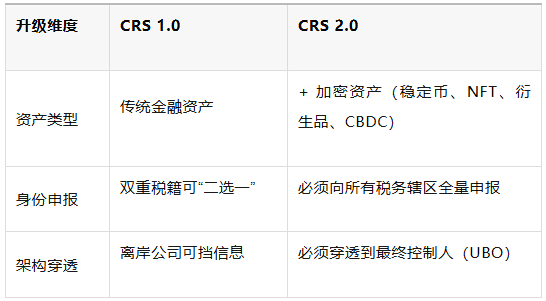

3. What has been upgraded in CRS 2.0? CRS 2.0 is a major upgrade based on 1.0, involving three aspects:

At the same time, the penalties have been significantly increased: Failure to report can result in fines per account, and severe fraud can incur a maximum fine of 500,000 Hong Kong dollars, and criminal liability can also be pursued.

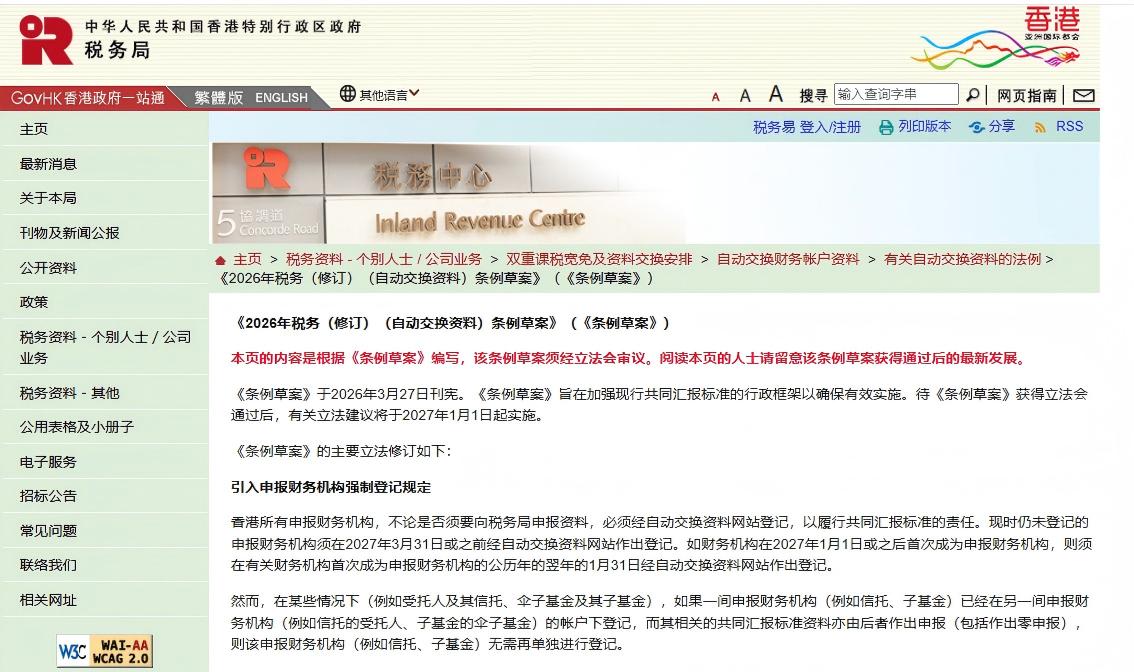

4. Timeline (Hong Kong) March 2026: The government publishes the legislative draft through a formal proclamation. April 2026: Submission of the first reading to the Legislative Council January 1, 2027: The regulations come into effect, and cryptocurrency service providers begin to collect customer information. 2028: First Cross-border Exchange of Cryptocurrency Information 2029: Full implementation of CRS 2.0 for comprehensive exchange The global framework came into effect on January 1, 2026, and Hong Kong is also proceeding with the implementation simultaneously.

II. What exactly did CRS 2.0 bring about? Change 1: All crypto assets are now subject to reporting Before: The Hong Kong Stock Exchange bought Bitcoin, stored USDT, and invested in NFTs, but the tax authority couldn't see them. Now: All are included under the definition of financial assets. Which entities are required to submit? Licensed cryptocurrency exchanges (such as HashKey, OSL, etc.) Wallet custody service providers Cryptocurrency payment institutions Which assets need to be declared? Stablecoins (such as USDT, USDC, DAI, etc.) NFTs with investment attributes (such as those with royalty and profit distribution functions) Crypto asset derivatives (futures, options) Central bank digital currencies (CBDC) A point that is often overlooked: Even if you mainly use decentralized exchanges, as long as you have conducted any operations through centralized entry points (such as fiat currency deposits or cross-chain bridge conversions), the information on that path may still be recorded. Self-deployed wallets do not report this information themselves, but once they interact with the exchange, traces are left behind.

Change 2: Dual tax residents are prohibited from choosing "either one" Previously: People who were both tax residents of the mainland and Hong Kong could fill out the form at the bank and simply select "I am a Hong Kong resident", and the bank would no longer report this information to the mainland. Now: Once a bank discovers that you have multiple tax resident statuses, it must report to all relevant jurisdictions. It does not accept the option of "choosing only one". Impact: Your account information will be stored simultaneously in the computer systems of both the mainland tax authority and the Hong Kong tax authority. But note: The information being seen by both sides ≠ Both sides having to pay taxes. The allocation of taxing rights is still determined by the "Arrangement for Avoidance of Double Taxation between the Mainland and Hong Kong". The criterion remains the "Gabi rule": permanent residence → important interest center → habitual residence → nationality. So: The Gabi rule has not failed; it has merely shifted from "bank counters" to "government meeting rooms".

Change 3: Offshore structures are being exposed, and shell companies are no longer secure Before: Holding Hong Kong accounts through offshore companies like BVI or Cayman Islands, financial institutions only saw the company names. Nowadays: Financial institutions must identify and register the ultimate controller (UBO), even if you hold an investment entity (such as a fund or trust), you must trace back to the natural person. Consequence: The "privacy barrier" of shell companies has completely vanished. Your personal tax information will be directly reported to the tax authority of your home country. A common misconception: Some people think that "my BVI company has independent legal person status and the bank won't penetrate it." Wrong. CRS 2.0 clearly stipulates that "it is necessary to penetrate the legal form and identify the ultimate controller."

III. Impact on Different Groups and Suggestions for ResponseTo make it clearer for you, I will explain based on five typical identities:

1. Pure mainland tax resident (without Hong Kong identity) Characteristics: Resided in mainland for more than 183 days, without Hong Kong ID card, has a Hong Kong account or crypto assets. Impact of CRS 2.0: Hong Kong account information → Exchanged with the mainland tax authority Cryptocurrency transaction records (such as on compliant exchanges in Hong Kong) → Will also be exchanged Will there be an increase in tax payment? No. The mainland has always levied taxes on global income. It's just that it might not have been possible to detect it before. Now that it can be detected, one needs to voluntarily report it. Risk point: Unreported overseas income in the past may result in tax re-payment and penalties. Recommendations for Response: Review all overseas financial accounts and crypto assets Actively make supplementary tax declarations to the mainland tax authorities Avoid the mentality of侥幸 (taking the easy way out)

2. Pure Hong Kong tax resident (without mainland tax registration) Characteristics: Mainly reside in Hong Kong, have not lived in the mainland for 183 days, may have given up the mainland residency. Impact of CRS 2.0: The information was exchanged with the Hong Kong Tax Bureau. However, Hong Kong does not levy income tax or capital gains tax on foreign earnings. It has no actual impact on the tax burden for most people. Risk points: If you have an offshore structure (such as BVI) under your name, be sure to make the穿透申报. If you hold crypto assets and trade them through an exchange, make sure to fulfill the reporting obligation. Recommendations Regularly update the tax resident declarations of banks and exchanges Examine whether the offshore structure needs to be retained

3. Mainland-Hong Kong dual tax residents Characteristics: Both regions have residence traces, the number of days of residence in each place may be close to or exceed 183 days each year, and they hold assets in both regions. Impact of CRS 2.0: The account information is simultaneously reported to both the mainland and Hong Kong tax authorities. However, the taxing authority is determined by the China-Hong Kong tax treaty, and there will be no double taxation. The real risk: Previously, it might have been "neither side reported" or "only reported one side". Now this option is blocked. If the truth is still concealed, it will be regarded as a false declaration and face investigation and fines. Recommendations for response: Objective assessment of one's "true tax resident status" (determine which side one's life focus is on) Make a truthful declaration of all identities to financial institutions Prepare materials to prove the "life focus" (residence records, family, work, etc.) If both sides meet the resident criteria, be prepared for inquiries but don't worry about double taxation.

4. Holding a Hong Kong account through an offshore company Characteristics: Register a BVI or Cayman company, use the company to open an account in Hong Kong, and the individual is the ultimate controller. Impact of CRS 2.0: Financial institutions must drill down to the individual and directly submit your information. The "shield" of shell companies has become ineffective. Recommendations for response: Option A: Inject real business substance into the offshore company (offices, employees, actual business decisions, meeting records) Option B: Shut down the shell company and place the assets under the individual's name or a compliant Hong Kong company Don't hold onto the illusion that "the company can block information"

5. People holding crypto assets (regardless of identity) Characteristics: Hold stablecoins, NFTs, crypto derivatives, or have conducted compliant transactions in Hong Kong. Impact of CRS 2.0: Starting from 2027, exchanges and custodian institutions begin to collect information. Starting from 2028, cross-border information exchange begins. Risk points: Never reported the income from crypto assets, and it may be traced in the future. Through centralized entry points (foreign currency deposit, exchange conversion), the records will be retained. Recommendations: Sort out all holdings and transaction records of crypto assets (including cancelled accounts) Record the addresses of self-depository wallets and their interaction history Confirm which NFTs are considered to have "investment attributes" Evaluate whether it is necessary to proactively file with the tax-resident country The period before 2027 is the final window for active adjustments

Four. The five things you should do now (Practical Checklist) Do not panic and cancel your account or rush to transfer your assets. Follow the steps below to handle the situation in an orderly manner:

Step 1: Confirm your tax resident status Don't rely on intuition. Compile a record of your activities over the past three years: The number of days of residence in each country/region Permanent residence address Location of family members Location of main business activities Location of social security, medical care, and tax records Judgment criteria: Only if one side exceeds 183 days → Tax resident of that country If both sides exceed 183 days → Dual tax resident (need to report to both sides, but don't worry about double taxation)

Step 2: Sort out your "information exposure" List all the: Hong Kong and other overseas bank accounts Securities/Funds/Insurance accounts Crypto asset exchange accounts (even if they have been closed) Managed wallet accounts Accounts held by offshore companies For each account, confirm: Is the tax resident declaration filled out at the account opening still accurate? Is an update necessary?

Step 3: Update all financial institution self-declarations Log in to your online banking or contact your account manager to update your tax resident information. Active update > Marked by the system as "inconsistent information".

Step 4: Review the Offshore Structure If your BVI/Cayman Islands company: No independent office No local employees No actual business decisions → It is just a "shell". Either inject substance (by increasing compliance costs annually), or shut down. Don't wait to be penetrated before responding.

Step 5: Specialized Review of Cryptocurrency Assets Export your transaction records from all exchanges (in CSV format) Record your self-hosted wallet addresses and interaction history Confirm which NFTs are considered to have "investment attributes" Evaluate whether active declaration is necessary Advice: If you hold a large amount of cryptocurrency assets, consult with professionals who are familiar with the subject. Do not make guesses on your own.

V. Quick Reference Guide for Common Issues

Final Words CRS 2.0 is not a surprise; it is a global tax transparency upgrade that was announced long ago. It will not make you pay an extra tax, nor will it harm your legitimate wealth. It does only one thing: it makes the past arrangements that relied on information asymmetry to "get away with it" no longer feasible. For legally and compliant wealth, transparency actually serves as protection, providing a clearer basis for your tax planning. We hope this article helps you move from "hearing about it" to "knowing about it".

Declaration: The content of this article is sourced from the internet and is provided for sharing and reference only. The copyright of the article belongs to the author and the original source. Reproduction is prohibited without the permission of the original author. If there are any copyright issues, please contact the backend for deletion.

Shengsen International Business Since its establishment in 2012, Shengsen International Business has accompanied over 100,000 enterprises in completing the compliance overseas expansion from the mainland to Hong Kong and then to the global market, providing full-cycle one-stop services. Why choose Shengsen? Professional team: 100+ senior tax and compliance advisors, with 70% of the members having over 8 years of industry experience. Dual-headquarters advantage: Dual headquarters in Hong Kong and Shenzhen, with physical operations, efficient and transparent service response Compliance qualifications: Hong Kong TCSP licensed secretarial company + accounting firm, providing a complete chain of compliance services Banking resources: Deeply cooperate with over 30 international banks to facilitate the efficient opening of Hong Kong accounts. Experience endorsement: Have served over 100,000 enterprises, with an annual audit pass rate of 100% and a customer retention rate exceeding 96% Full-service solution: registration, account opening, auditing, tax filing, and architecture setup - all in one, providing a comprehensive solution to cross-border challenges.

Compliance is no trivial matter. Professional matters should be entrusted to professionals. For consulting services, please scan the QR code below 👇 or call (15302790432, the same number for WeChat), and we will arrange a senior cross-border tax and finance consultant for you to provide one-on-one professional interpretation and customized solutions.